With 2022 behind us, Gower Street is once again taking a look ahead to what’s on the horizon for this year.

The past year brought further recovery but also challenges for the global box office: A depressed Chinese box office (ending nearly $3bn behind 2021); the Russian invasion of Ukraine and resultant US studio boycott of Russia; an exchange rates rollercoaster ultimately reducing the US$ figure coming from international markets by $1bn+; and a release calendar with large gaps exacerbated by a host of titles moving out of 2022 (removing $1bn+ from our Domestic estimate alone). Can we expect better things in 2023?

Gower Street’s first Global Box Office prediction for 2023 suggests further improvement. The $29 billion projection would represent a 12% gain over the current year if 2022 remains on course for an approximate $25.8 billion global box office (Gower Street measures it stood at $23.6 billion as of December 10). The year-on-year gain will be smaller than that seen this year (est. +21% is US$ terms), though this is to be expected as global box office continues its recovery.

This projection, calculated utilizing data from Gower Street’s flagship FORECAST service and analyst assessment, is based on the current release calendar. It should be noted that this is a very early prediction and Gower Street would expect to see further changes to the release calendar result in some fluctuation. It can also not account for unexpected global events.

If the projection holds it would suggest the industry will need to wait until at least 2024 to see a full return to pre-pandemic global box office levels. Our 2023 forecast is still 27% behind the average of the last three pre-pandemic years (2017-2019) at current exchange rates (this would rise to 30% compared to historic rates).

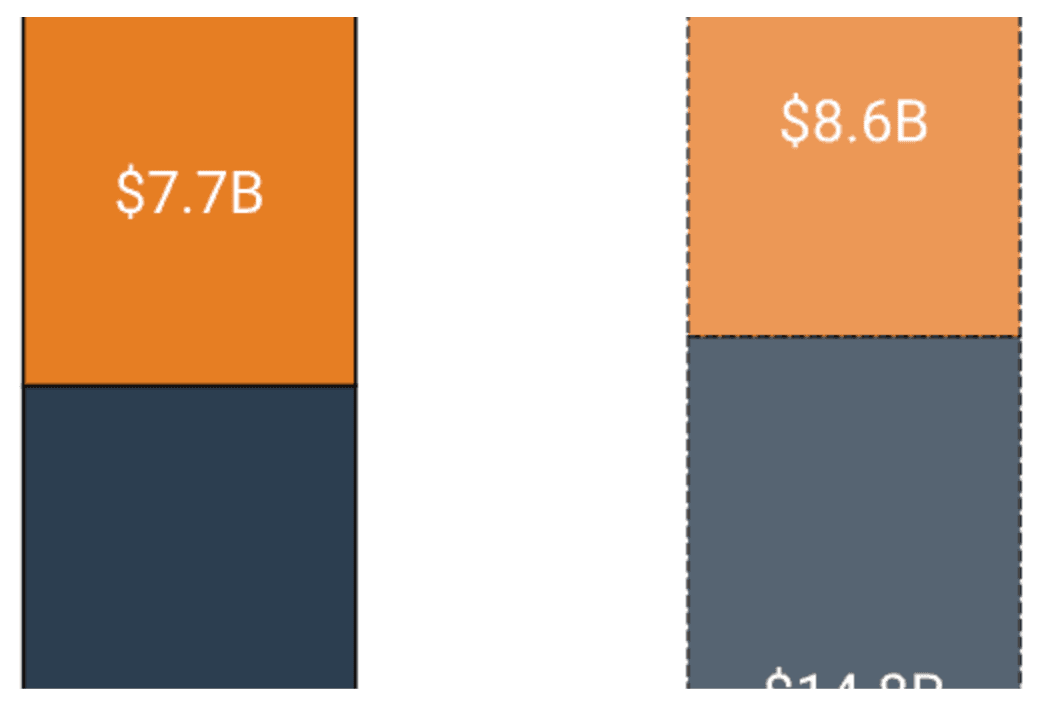

The Domestic market is projected to deliver a 12% increase in 2023 ($8.6bn) over 2022 ($7.65bn) but come in 25% behind an average of the last three pre-pandemic years. The Asia Pacific (exc. China) and Latin America regions are both expected to gain 11-12% on 2022 and come in approximately 20% down on the pre-pandemic average. The Europe, Middle East and Africa region is expected to increase approximately 7% on 2022 and finish 30% behind the pre-pandemic average (the key impact here is Russia). With a lesser known advance release calendar and continued uncertainty around access for import titles and changing covid policy China remains the market that is hardest to predict. We are currently projecting $5.55 billion for China, a rise on 2022 but well short of its 2021 figure.